This in-depth TCS Q1 results analysis unpacks the numbers behind the headlines from July 10, 2025. The Street had its eyes glued to Tata Consultancy Services’ Q1 FY26 earnings, and as India’s IT crown jewel, TCS rarely fails to deliver surprises. This quarter was no exception. While the profit numbers had analysts celebrating, the revenue story painted a more complex picture that demands closer scrutiny from every investor.

The Profit Party: TCS Beats Street Expectations

TCS delivered a stellar performance on the bottom line, reporting a net profit of Rs 12,760 crore for the April-June quarter. This represents a solid 6% year-on-year growth that caught analysts off guard in the best possible way.

The consensus was expecting a much more modest performance. Bloomberg’s analyst poll had projected just 1.9% growth, estimating profits at Rs 12,263 crore. An ET report was even more conservative at Rs 12,205 crore. TCS didn’t just meet these expectations – it sailed past them with room to spare.

Adding sweetness to the deal, the company declared an interim dividend of Rs 11 per share. Shareholders can mark their calendars for August 4, 2025, as the payout date, with July 16 set as the record date.

The Revenue Reality Check: Growth Hits a Speed Bump

While profit margins celebrated, the revenue story tells a tale of caution. TCS posted revenue of Rs 63,437 crore, marking a modest 1.3% year-on-year growth. This figure fell short of the Bloomberg consensus estimate of Rs 64,636 crore.

The real concern in our TCS Q1 results analysis emerges when we examine the Constant Currency (CC) performance. (This metric removes the effect of currency exchange rate fluctuations to show a company’s underlying business performance). Here, revenue actually declined by 3.1% year-on-year – a red flag that suggests underlying demand weakness.

Quarter-on-quarter, the picture isn’t much brighter. Revenue dropped 1.6% from Q4 FY25’s Rs 64,479 crore, indicating that the challenges aren’t just year-over-year comparisons but reflect current market conditions.

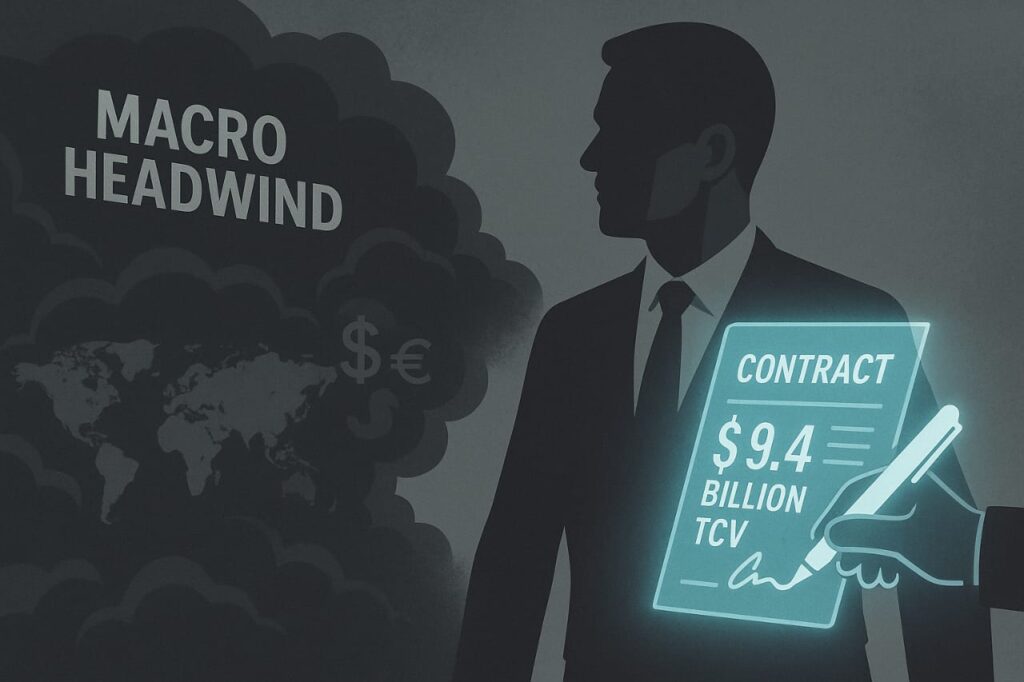

CEO Speaks: Macro Headwinds Take Center Stage

TCS CEO K Krithivasan didn’t mince words about the challenging environment. “The continued global macro-economic and geo-political uncertainties caused a demand contraction,” he stated, acknowledging the elephant in the room.

However, it wasn’t all doom and gloom. The CEO highlighted that new services demonstrated strong growth and the company secured “robust deal closures during this quarter” with a Total Contract Value (TCV) of $9.4 billion. (TCV represents the total value of a contract, and strong TCV can be an indicator of future revenue. For more on this, see this Gartner TCV explanation).

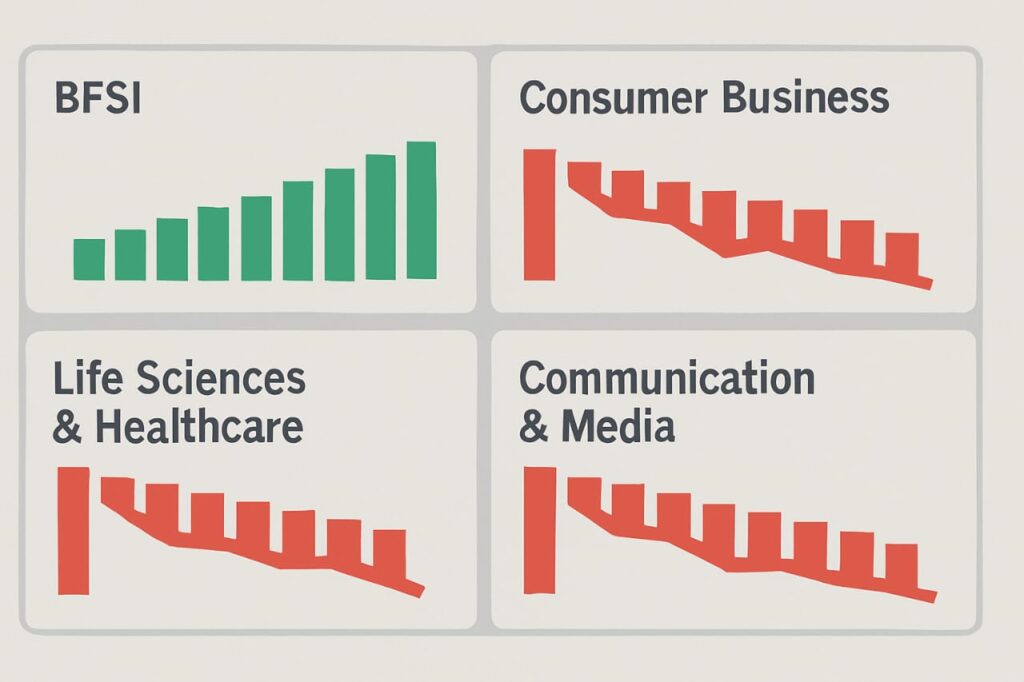

Sector Performance: Winners and Losers Emerge

The segmental breakdown reveals a mixed bag of performance across different industries:

The Steady Performers

- BFSI (Banking, Financial Services, and Insurance): The backbone of TCS showed resilience with 1% YoY growth in CC terms, contributing 32% to total revenue.

- Technology & Services and Energy sectors: Both recorded positive year-over-year growth.

The Struggling Segments

- Consumer Business: The second-largest revenue contributor saw a 3.1% YoY decline, accounting for 15.6% of Q1 FY26 revenue.

- Life Sciences & Healthcare: Recorded the steepest decline at 9.6% year-over-year.

- Communication & Media: Matched the healthcare sector’s decline at 9.6% YoY.

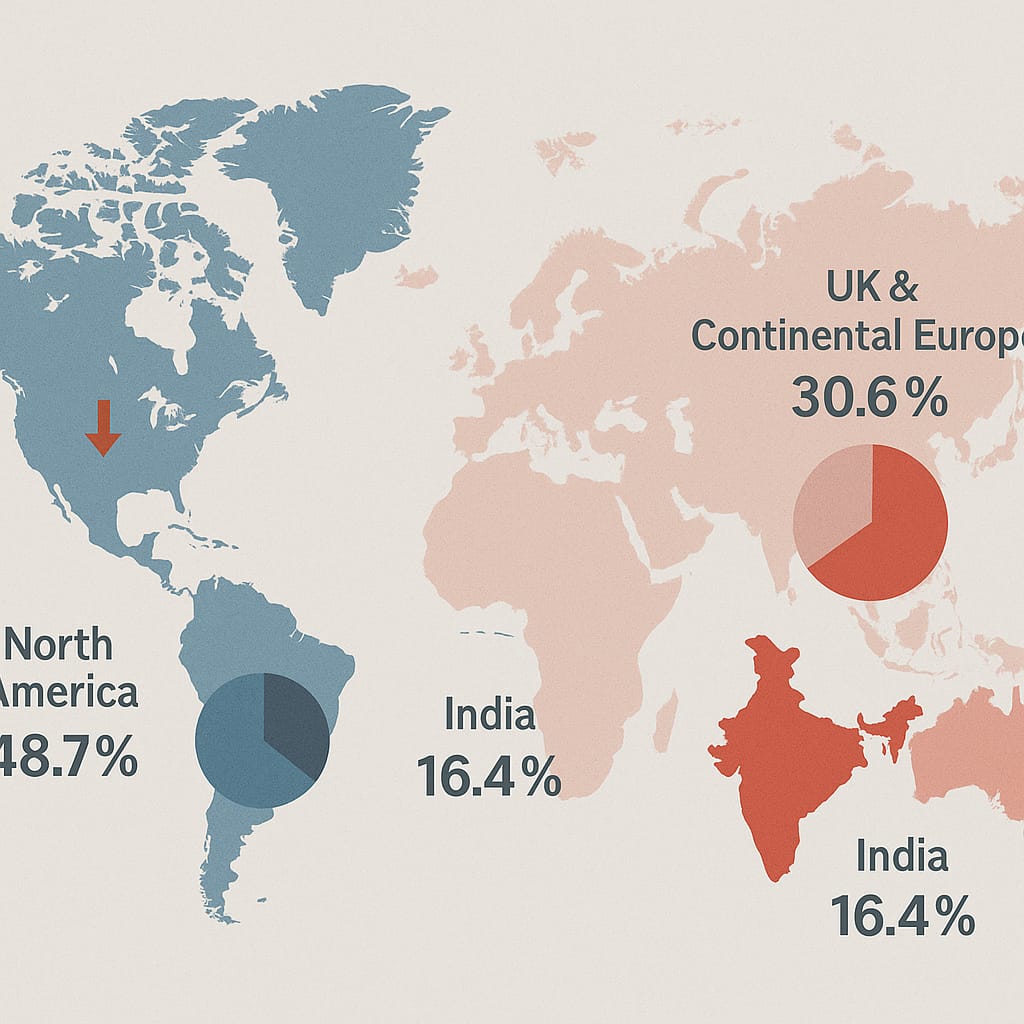

Geographic Mix: North America Remains Dominant but Shrinks

The geographical revenue distribution shows North America’s continued dominance, though with some concerning trends:

- North America: Market share decreased to 48.7% (down 2.7% YoY).

- UK: Operations declined by 1.3%, reaching 18% of total revenue.

- Continental Europe: Fell by 3.1% to 15% of total revenue.

- India: Domestic share reduced to 5.8%, showing a significant 21.7% YoY decline in CC.

The People Factor: Attrition Rises, Salary Hikes on Hold

TCS’s workforce reached 613,069 employees as of June 30, 2025, with a net addition of 6,071 year-over-year. The company hired over 5,000 employees during the quarter, showing confidence in future growth.

However, the attrition rate climbed to 13.8% from 13.3% in Q4 FY25. (Attrition rate measures the percentage of employees who leave a company over a specific period). This is above TCS’s comfort level of 13%, with Chief Human Resources Officer Milind Lakkad acknowledging efforts to bring it down.

Perhaps more telling is the continued delay in wage hikes. Lakkad confirmed that TCS “has not made any decisions so far on the potential salary increase” – a decision that reflects the cautious approach management is taking given the uncertain business environment.

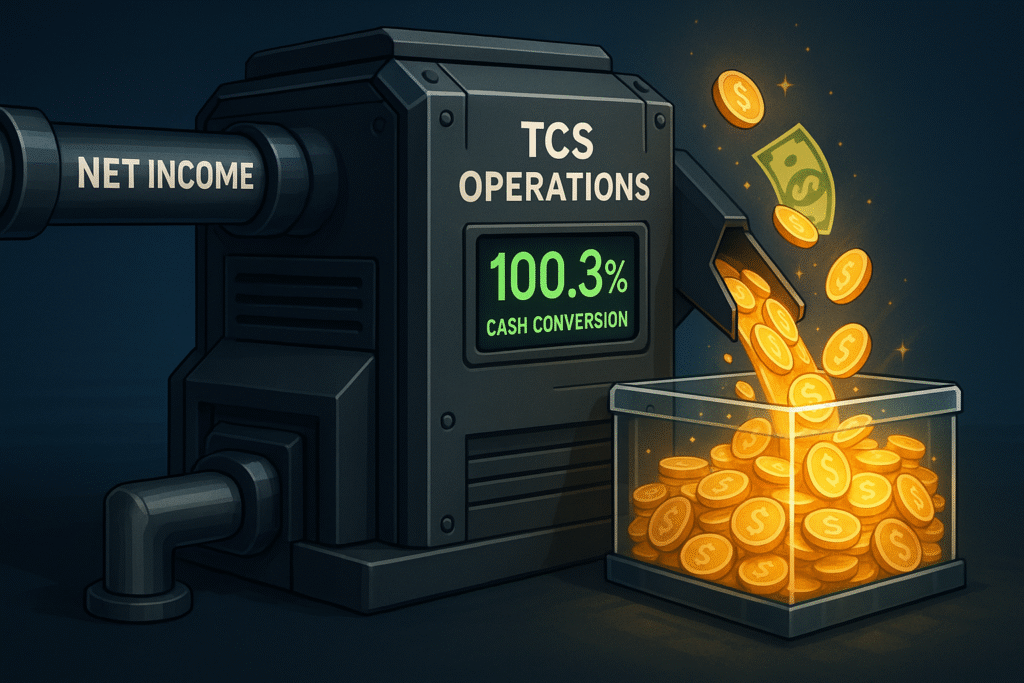

Financial Strength: Cash Generation Remains Robust

Despite revenue challenges, TCS demonstrated impressive operational efficiency:

- Net Margin reached 20.1% during the quarter.

- Generated Net Cash of Rs 12,804 crore, representing 100.3% of net income.

- Strong cash conversion provides financial flexibility for future investments.

The Road Ahead: Strategy in Uncertain Times

CEO Krithivasan outlined the company’s strategic focus: “We remain closely connected to our customers to help them navigate the challenges impacting their business, through cost optimization, vendor consolidation and AI-led business transformation.”

This approach suggests TCS is positioning itself as a partner for clients looking to manage costs while investing in digital transformation and AI adoption. (To understand how IT services help with cost optimization, read this Deloitte perspective).

The Verdict: Resilience Amid Headwinds

This TCS Q1 results analysis presents a classic case of operational excellence meeting market challenges. The strong profit performance and dividend declaration showcase the company’s ability to manage costs and maintain shareholder value. However, the persistent revenue headwinds, particularly in constant currency terms, highlight the impact of global uncertainties on demand.

The mixed segmental performance and rising attrition rates add layers of complexity to the narrative. For investors, the takeaway from this TCS Q1 results analysis is that while the company remains a fundamentally strong company, the revenue challenges suggest near-term growth may remain muted until global economic conditions improve.

The company’s focus on AI-led transformation offers hope for future growth, but the timeline for recovery depends largely on factors beyond TCS’s control.

Disclaimer: This analysis is based on publicly available information and is intended for informational purposes only. It should not be construed as financial advice or a recommendation to buy, sell, or hold any securities. Readers are advised to consult with qualified financial advisors and conduct their own research before making any investment decisions. Past performance does not guarantee future results.